For many buyers, home loan pre-approval feels like permission to start buying. It gives you a clearer budget, helps you speak to selling agents with more confidence and makes the property search feel more serious.

But pre-approval is not the same as full approval.

That difference matters, especially in Melbourne’s property market where buyers often need to make fast decisions, negotiate under pressure or bid at auction. If you treat pre-approval as guaranteed finance, you may commit to a property before the lender has fully accepted the loan and the property.

For first-time property investors and Melbourne buyers, understanding pre-approval vs approval can help reduce finance risk before making an offer.

What Is Pre-Approval?

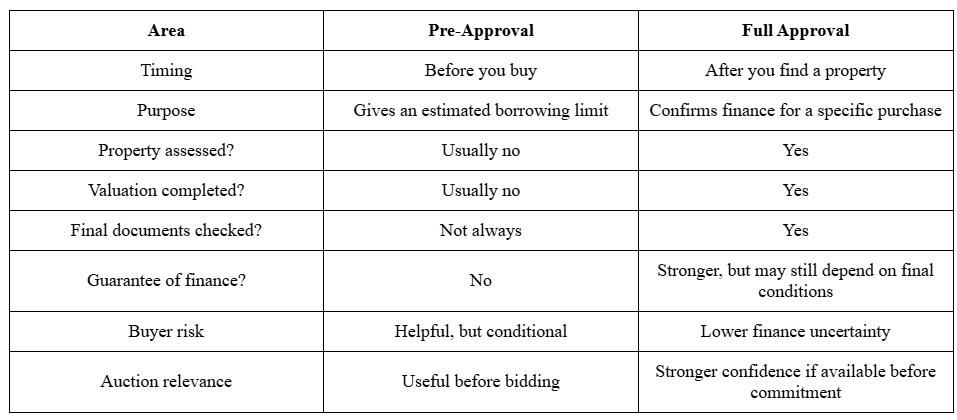

Pre-approval, also known as conditional approval or approval in principle, is an early indication from a lender that you may be able to borrow up to a certain amount.

The lender usually reviews your income, expenses, savings, deposit, credit history and existing debts. Based on this information, they may provide an estimated borrowing limit.

NAB explains that home loan pre-approval means a lender has agreed in principle to lend money, but it has not progressed to full and final approval. NAB also notes that pre-approval does not guarantee unconditional finance approval.

Pre-approval can help buyers understand:

- How much they may be able to borrow

- What price range to search in

- Whether their deposit is likely to be sufficient

- Whether their finances broadly meet lender requirements

- Whether there are early borrowing concerns to resolve

It is useful, but it is still conditional.

What Is Full Approval?

Full approval is a later stage in the home loan process. It usually happens after you have found a property and the lender has assessed the final details.

This may include:

- The signed contract of sale

- The property valuation

- Updated income documents

- Final credit checks

- Deposit confirmation

- Loan structure

- Any lender-specific conditions

Full approval means the lender has assessed both you as the borrower and the property as security for the loan.

This is why full approval carries more weight than pre-approval. It is closer to the lender confirming that the loan can proceed, subject to any remaining formal steps.

What Is the Difference Between Pre-Approval and Full Approval?

The main difference is that pre-approval is mostly about your borrowing position, while full approval considers both your borrowing position and the specific property.

In simple terms, pre-approval helps you search. Full approval helps you settle.

Why Pre-Approval Matters for Melbourne Buyers

Pre-approval is still important. It gives buyers a realistic starting point before inspecting properties or making offers.

For Melbourne buyers, pre-approval can help with:

- Setting a clear property budget

- Avoiding inspections outside your price range

- Speaking to selling agents with more confidence

- Moving faster when the right property appears

- Understanding deposit and repayment expectations

- Planning before auction campaigns

Melbourne buyers often deal with competitive private sales, tight campaign timelines and auction pressure. Without a clear finance position, it is easy to emotionally stretch beyond a comfortable limit.

Why Pre-Approval Is Not Enough

Pre-approval does not remove all finance risk.

A lender may still decline, reduce or delay approval if:

- Your financial situation changes

- Your income documents are outdated

- Your expenses are reassessed

- Interest rates change

- The property valuation is lower than the purchase price

- The property type does not meet lender criteria

- There are issues with the contract

- The lender changes its credit policy

- The deposit source is not accepted

This is why buyers should not treat pre-approval as a final yes.

A property may fit your pre-approved limit, but the lender may still have concerns about that specific property.

Pre-Approval and Auctions in Melbourne

Auction buying is where the difference between pre-approval and full approval becomes especially important.

Consumer Affairs Victoria advises buyers to arrange pre-approved finance before auction. It also notes that if you buy at auction, you cannot make the contract of sale subject to finance without the vendor’s agreement.

This means the risk sits with the buyer.

If you win at auction and the lender later reduces the loan due to a valuation issue or final assessment, you may need to find extra funds. That can create serious settlement pressure.

Before bidding at auction, buyers should:

- Confirm their borrowing position with a broker or lender

- Review the contract and Section 32

- Understand the deposit required on auction day

- Check whether the lender has any concern with the property type

- Discuss valuation risk before bidding

- Set a strict walk-away price

- Avoid bidding beyond their approved comfort level

Consumer Affairs Victoria also recommends getting independent expert help on legal, finance and building matters before bidding and deciding your bidding limit before auction.

What Buyers Should Check Before Making an Offer

Before making an offer, buyers should ask their broker or lender:

- Is my pre-approval current?

- Is it fully assessed or system-generated?

- What documents still need to be updated?

- Does the property type meet lender requirements?

- What deposit do I need ready?

- Can I include a finance clause?

- How long will full approval take?

- What happens if the lender valuation is lower than the purchase price?

- Are there any risks with my income, expenses or loan structure?

For private sales, buyers may be able to negotiate conditions such as subject to finance, building inspection or pest inspection. Consumer Affairs Victoria notes that private sale contracts can be made subject to conditions such as loan approval, sale of an existing property, or successful building and pest inspection.

What Investors Need to Consider

For first-time property investors, loan approval is only one part of the decision.

A lender may approve the loan, but that does not automatically mean the property is a good investment.

Investors should also check:

- Expected rental income

- Vacancy risk

- Loan repayments

- Interest rate buffers

- Owners corporation fees

- Land tax considerations

- Insurance

- Maintenance costs

- Future borrowing plans

- Whether the purchase supports the next investment step

This is where buyers should move from “Can I buy it?” to “Should I buy it?”

A property that fits the approved loan amount may still create cash flow pressure if the rent is weak, holding costs are high or repairs are likely.

Common Mistakes Buyers Make

Many buyers misunderstand pre-approval because it feels more final than it really is.

Common mistakes include:

- Assuming pre-approval guarantees finance

- Bidding at auction without understanding valuation risk

- Letting pre-approval set the maximum bid instead of a comfortable limit

- Forgetting to update expired pre-approval

- Changing jobs, debts or spending before full approval

- Making an unconditional offer without finance confidence

- Ignoring the property type or lender policy risk

The safest approach is to keep finance advice current throughout the buying process.

How a Buyer’s Agent Can Help

A buyer’s agent does not replace a broker, lender or conveyancer. However, they can help connect the finance position with the property strategy.

For Melbourne buyers, a buyer’s agent can help:

- Search within a realistic budget

- Avoid properties that do not match the investment brief

- Compare recent sales before making an offer

- Reduce the risk of emotional overbidding

- Support auction planning

- Coordinate checks before purchase

- Assess whether the property suits long-term goals

- Help buyers stay disciplined when competition increases

This can be especially useful for first-time investors who have pre-approval but are unsure how to use it safely in a live property search.

Final Thoughts

Pre-approval and full approval are not the same thing.

Pre-approval helps you start the search with more confidence. Full approval provides stronger confirmation once the lender has reviewed the property, valuation and final documents.

For Melbourne buyers, the key is to use pre-approval as a guide, not a guarantee. It should shape your budget, narrow your search and support better decisions, but it should not encourage you to overbid or ignore finance risk.

A good purchase should work financially before it works emotionally.

FAQs

Q. What is the difference between pre-approval and full approval?

A. Pre-approval is an early indication of how much you may be able to borrow. Full approval comes later, after the lender has assessed the property, valuation and final loan documents.

Q. Is pre-approval the same as approval?

No. Pre-approval is usually conditional and does not guarantee final loan approval. Full approval is a more complete stage of the lending process.

Q. Does pre-approval guarantee a home loan?

No. Pre-approval does not guarantee a home loan. The lender may still reassess your finances, the property valuation and the final loan conditions.

Q. Can I make an offer with pre-approval?

Yes, many buyers make offers with pre-approval. Where possible, buyers should consider a finance clause and confirm their position with a broker or lender first.

Q. Can I bid at auction with pre-approval?

Yes, but there is risk. Auction contracts are usually unconditional, so buyers should confirm their borrowing position, understand valuation risk and set a strict bidding limit before auction.

Q. What happens if valuation is lower than the purchase price?

If the lender valuation is lower than the purchase price, the lender may reduce the loan amount. The buyer may need to contribute more deposit, renegotiate if possible, or review their options with their broker.

Q. How long does pre-approval last?

Pre-approval usually lasts for a limited period, often around three to six months depending on the lender. Buyers should check the exact expiry date with their broker or bank.

Q. Can full approval be declined after pre-approval?

Yes. Full approval can still be declined if your financial situation changes, documents are incomplete, the valuation is low or the property does not meet lender criteria.

Q. Should investors rely only on pre-approval?

No. Investors should also review rental income, vacancy risk, loan repayments, holding costs, tax considerations and whether the property supports their wider investment strategy.

Q. Can a buyer’s agent help with pre-approval?

A buyer’s agent does not arrange loan approval, but they can help you search within a realistic budget, assess property value and avoid overbidding based on emotion.