Interest rates do more than change monthly repayments. They influence how much investors can borrow, what type of property they can afford, how much cash flow they need, and how confidently they can hold an asset over time.

For Melbourne investors, this can shape almost every part of the buying decision. It can affect suburb choice, property type, rental yield expectations, negotiation strategy and the timing of the next purchase.

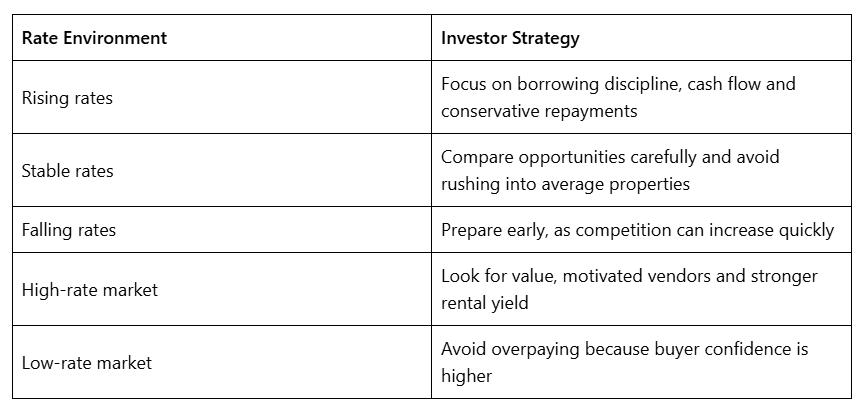

When rates rise, investors usually become more cautious. When rates fall, buyer confidence often improves and competition can return quickly. The challenge is not trying to perfectly time the market. The smarter approach is to understand how interest rates affect property investment strategies and build a plan that can hold up across different market conditions.

As of May 2026, the RBA’s May Statement on Monetary Policy noted that market pricing assumed the cash rate could increase to 4.70% by the end of 2026. This makes interest rate planning a key consideration for anyone buying an investment property in Melbourne.

How Interest Rates Impact Property Prices

Interest rates impact property prices by changing borrowing power, buyer demand and market confidence.

When interest rates are lower, buyers can usually borrow more. Repayments are more manageable, which can increase competition for property. This can place upward pressure on prices, especially in suburbs where supply is limited.

When rates rise, the opposite can happen. Borrowing power falls, repayments increase and some buyers step back from the market. This can reduce competition and slow price growth.

However, higher interest rates do not automatically mean property prices will fall everywhere. Property prices are also shaped by housing supply, population growth, employment, rental demand, suburb appeal and property type.

In Melbourne, this matters because the market is not uniform. Inner-city apartments, townhouses in middle-ring suburbs and family homes in established school zones can all respond differently to rate changes.

Recent market reporting has shown softer conditions in Melbourne, with dwelling values declining 0.6% in April 2026 and sitting 2.3% below their March 2022 high.

What Rising Interest Rates Mean for Melbourne Investors

For investors, rising rates usually create three main pressures: lower borrowing power, higher holding costs and tighter cash flow.

A first-time investor may find that their approved budget is lower than expected. A rentvestor may need to balance their own rent with investment loan repayments. A portfolio builder may need to wait longer before buying the next property because equity access or serviceability has reduced.

In Melbourne, this can influence whether an investor targets:

- A house in a growth corridor

- A townhouse in a middle-ring suburb

- An apartment with stronger rental yield

- A smaller property in a better-connected location

- A suburb with more affordable entry prices

- A property with lower maintenance and holding costs

This is where strategy becomes important. A higher-rate market can reward disciplined buyers who understand their numbers and avoid emotional decisions.

How Interest Rates Affect Borrowing Power

Higher interest rates usually reduce borrowing capacity because lenders assess whether borrowers can afford repayments under current and stressed conditions.

For example, if an investor planned to borrow $750,000, a rate increase can make that loan more expensive to service. Even if the investor still earns the same income, the lender may approve a lower amount because the repayment burden is higher.

This can change the investment brief. Instead of stretching for a detached house in a highly competitive suburb, the investor may need to consider a townhouse, apartment or different suburb with a stronger balance between price, rent and long-term demand.

This is not always a bad thing. Tighter borrowing conditions can help investors stay disciplined and avoid buying a property that becomes difficult to hold.

How Interest Rates Affect Rental Yield and Cash Flow

Interest rates directly affect cash flow.

If repayments increase but rent does not rise at the same pace, the property becomes more expensive to hold. This is why rental yield becomes more important in a higher-rate environment.

Investors should look beyond the purchase price and review:

- Expected weekly rent

- Vacancy risk

- Owners corporation fees

- Council rates

- Insurance

- Maintenance costs

- Land tax considerations

- Future repair costs

- Demand from local renters

A property with strong long-term growth appeal may still be a good investment, but the investor needs to understand the holding cost clearly. For first-time investors, this is one of the most important parts of the decision.

How Investors Should Adjust Their Strategy

Interest rates should shape the strategy, not replace it.

In a rising-rate environment, investors may need to reduce their budget, increase their deposit, prioritise stronger rental income or avoid properties with high ongoing costs.

In a falling-rate environment, investors may need to act faster because buyer confidence can return and competition may increase.

Should You Buy When Interest Rates Are High?

A high interest rate does not automatically mean you should avoid buying. It simply means the numbers need to be tested more carefully.

Buying in a higher-rate market can make sense if:

- The property has strong fundamentals

- The rent supports the holding cost

- The suburb has long-term demand

- The purchase price is fair

- You can manage repayments comfortably

- You are not relying on short-term price growth

- You have a clear investment plan

There can also be opportunity when rates are high. Some buyers step back, vendors may become more flexible and competition can reduce in certain parts of the market.

The risk is buying without enough buffer. If the loan is already tight at today’s rate, the property may become stressful to hold if costs increase further.

How a Buyer’s Agent Can Help in a Changing Rate Market

A buyer’s agent can help investors make clearer decisions when interest rates are changing.

For Melbourne investors, this may include:

- Comparing suburbs based on budget and investment goals

- Assessing fair market value before making an offer

- Avoiding emotional auction bidding

- Identifying areas with stronger rental demand

- Reviewing property type risks

- Understanding whether a property suits long-term portfolio goals

- Negotiating when buyer confidence is lower

This support can be useful for first-time investors, reintvestors and professionals building a portfolio who do not want to rely only on listing prices, selling agent advice or short-term market commentary.

Final Thoughts

Interest rates should shape your property strategy, but they should not replace it.

For Melbourne investors, the goal is not simply to buy when rates are low or avoid buying when rates are high. The goal is to buy the right property, in the right location, at the right price, with a loan structure and cash flow position that can handle changing conditions.

Investors who understand their numbers, choose the right property type and focus on suburbs with strong fundamentals are usually better placed to manage interest rate changes over time.

FAQs

Q. How do interest rates affect property investment strategies?

A. Interest rates affect property investment strategies by changing borrowing power, loan repayments, cash flow and buyer confidence. When rates rise, investors may need to reduce their budget, focus on stronger rental yield or choose a more affordable suburb.

Q. How do interest rates impact property prices?

A. Interest rates impact property prices by influencing buyer demand. Lower rates can increase borrowing power and competition, while higher rates can reduce borrowing capacity and slow buyer activity.

Q. Do higher interest rates always reduce property prices?

A. No. Higher rates can place pressure on prices, but property prices also depend on supply, population growth, rental demand, employment and suburb-level competition.

Q. What happens to property prices when interest rates rise?

A. When interest rates rise, some buyers can borrow less, which can reduce competition. This may slow price growth or create softer market conditions, but the impact varies by location and property type.

Q. Do lower interest rates increase property prices?

A. Lower interest rates can support property price growth because buyers may be able to borrow more and compete more actively. However, prices still depend on supply, demand and local market conditions.

Q. How do interest rates affect rental yield?

A. Higher interest rates increase loan repayments, which can reduce cash flow. This makes rental yield more important because investors need stronger rent to help cover holding costs.

Q. How do interest rates affect borrowing power?

A. Higher interest rates usually reduce borrowing power because lenders assess whether borrowers can afford higher repayments. This can reduce the amount an investor is approved to borrow.

Q. Is Melbourne property a good investment when interest rates are high?

A. Melbourne property can still be a good investment in a high-rate environment if the property has strong fundamentals, reliable rental demand, fair pricing and manageable holding costs.

Q. Should investors prioritise cash flow or capital growth during high rates?

A. During high-rate periods, cash flow becomes more important because holding costs are higher. However, investors should still consider long-term capital growth, suburb fundamentals and property quality.

Q. Can a buyer’s agent help investors during changing interest rates?

A. Yes. A buyer’s agent can help investors assess fair value, compare suburbs, avoid overpaying, review rental demand and choose properties that match their investment strategy.